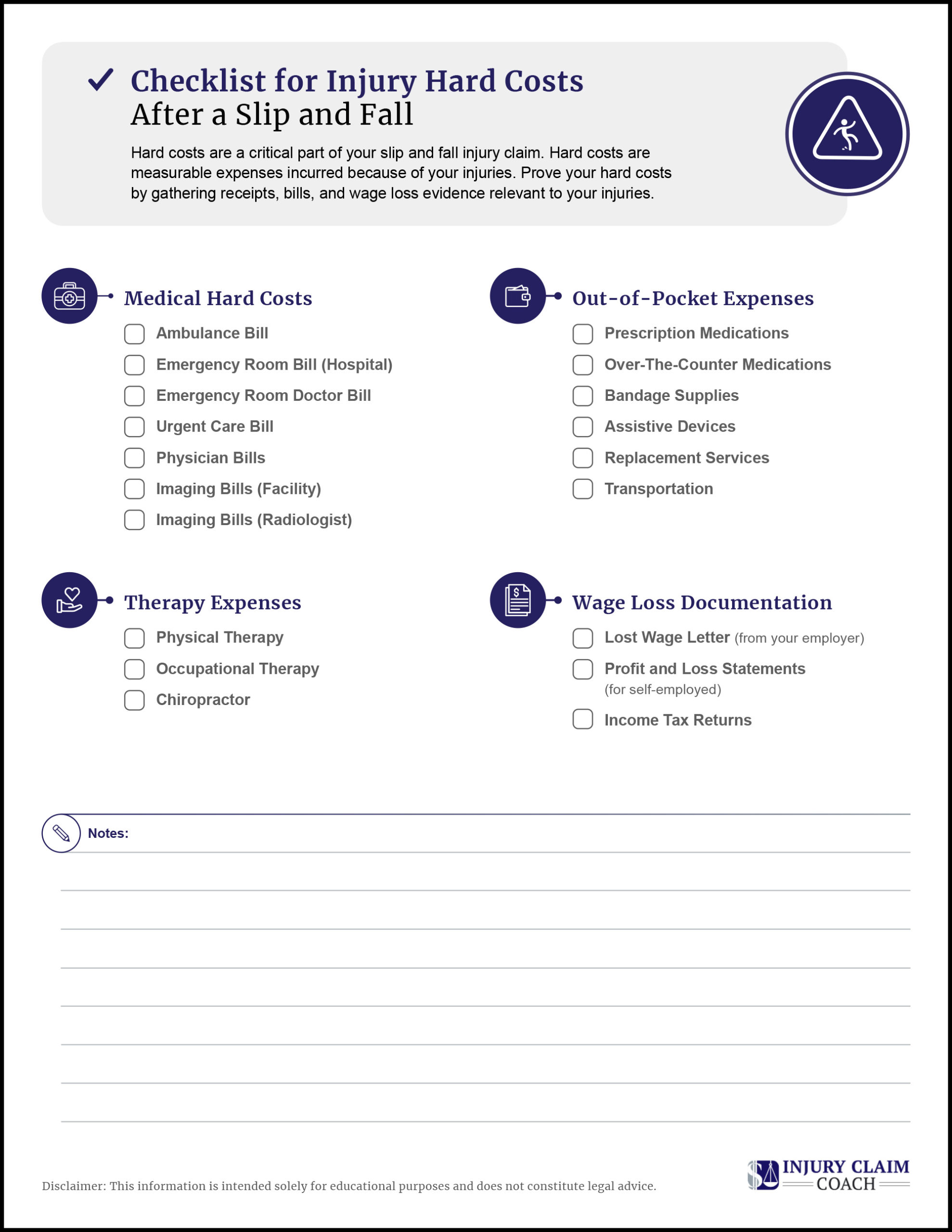

Maximize your slip and fall injury compensation with strong evidence. This checklist makes it easy to capture the hard cost evidence you need.

The value of your slip and fall injury is largely based on the total of your “hard costs” like medical bills and lost wages, with an amount added to account for your pain and suffering.

Don’t settle for less compensation than you deserve. Use this free checklist for Slip and Fall Injury Damages to be sure you’ve captured proof of your medical bills, lost wages, and out-of-pocket expenses.

Click on the image below to download the PDF checklist:

Hard Costs Lay the Foundation for a Strong Claim

The costs, expenses, and other financial losses you incur from a slip and fall injury are called hard costs. Insurance companies might also refer to hard costs as economic losses or “special damages” associated with your injuries. Hard costs are measurable, meaning there is a dollar value that comes from detailed bills, receipts, and wage statements.

Non-economic losses, commonly called pain and suffering, are often referred to as “general damages” by insurance adjusters.

When you’ve been injured because of a property owner’s negligence, you have a right to seek fair compensation for your hard costs – special damages- as well as your general damages. Most slip and fall claims are paid through the property owner’s insurance company.

Commercial properties, like grocery stores, hotels, and restaurants are covered by liability insurance policies. Private residences may be covered by homeowner’s insurance or a renter’s policy.

Hard costs are the foundation of a strong injury claim. You can calculate the value of your slip and fall injury claim by totaling your hard costs, and adding a multiple of that total to account for your pain and suffering.

If you overlook any medical bills or other hard costs before calculating your claim value, you risk selling yourself short. Once your injury claim is settled, the insurance company doesn’t owe you another penny. Using a Hard Costs Checklist can help you make sure you haven’t missed any reimbursable expenses.

Demand the Full Cost of Medical Treatment

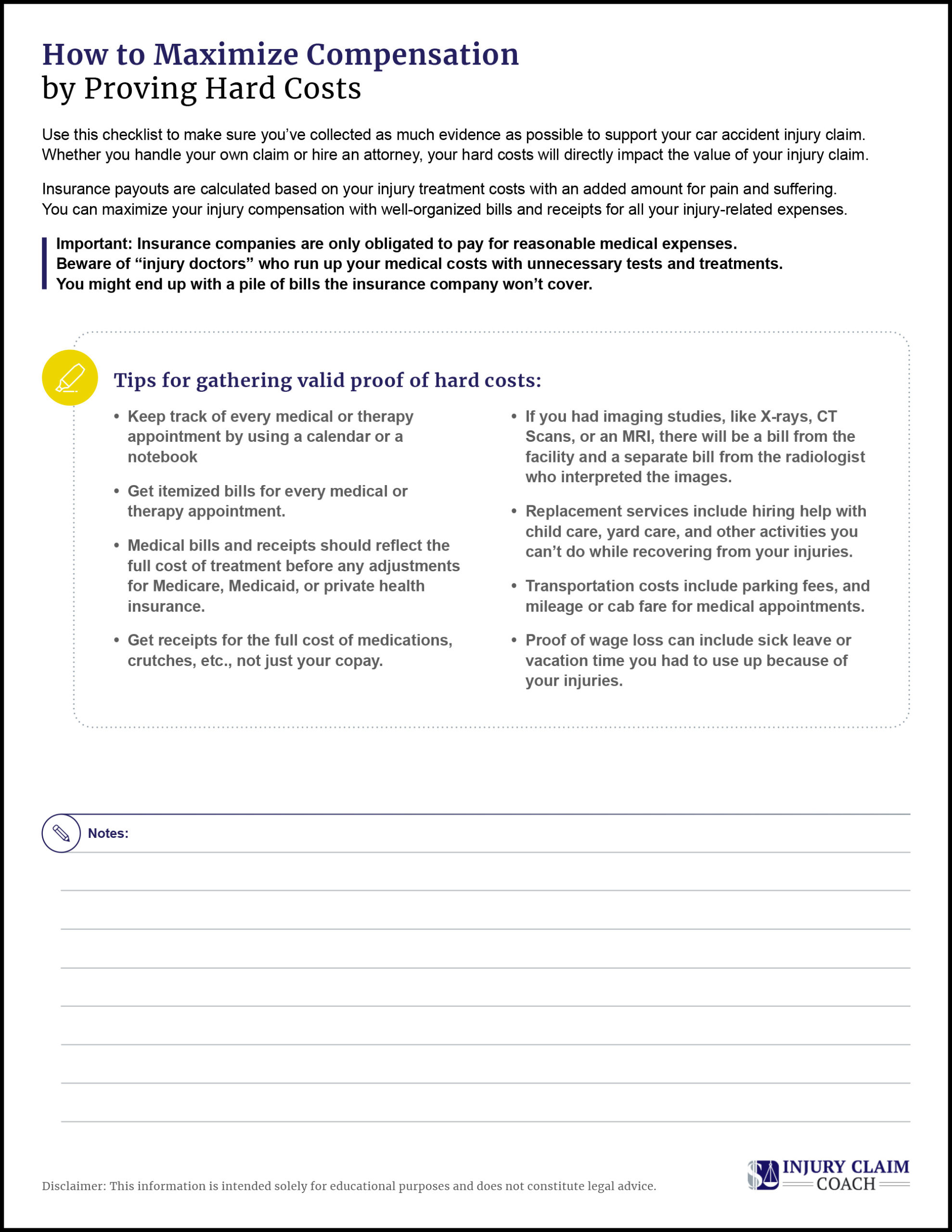

When it’s time to prepare your demand letter to the insurance company, ask for the full cost of your medical bills, before any adjustments for Medicare, Medicaid, or other health insurance. Don’t include your copay, because that amount would have been paid toward the full amount of the medical bill, not in addition to it.

For example, imagine you end up with a broken wrist after a slip and fall at a grocery store. You went to urgent care, had X-rays and your wrist was put in a cast. The doctor charges $400 to examine you and put your arm in a cast. When the bill comes, it shows your health insurance company paid $300, leaving you with $100 to pay for your copay and deductible. Your demand to the insurance company should include the full $400 cost of the doctor’s bill.

Likewise, be sure to get copies of bills for the full cost of prescribed medications and assistive devices, even if your health insurance covered part or all of the cost.

Be aware that Medicaid, Medicare, the VA, and private health insurance companies have the right to put a medical lien against your injury settlement to recover the amounts they paid on your behalf. So make sure you get enough from your car insurance claim to cover the full cost of your medical care, even if it didn’t come out of your pocket or the bill hasn’t been paid yet.

You will have multiple bills for hospital visits and diagnostic tests, like X-rays. Imaging tests like an X-Ray or CT Scan will generate a bill from the radiology center, and another bill from the radiologist who read the images and made the diagnosis.

If you are transported to a hospital emergency room, you can expect to get separate bills from the hospital, the ER doctor, and from the ambulance service.

Using a calendar or day planner can make it easier to keep track of all your medical and therapy appointments. When you’re ready to figure out the value of your injury claim, go through your calendar and make sure you have bills corresponding to each of your appointments.

Some bills will list more than one date of service. If you needed to have physical therapy three times a week for six months, you might have bills that show multiple treatment dates. It’s okay to use those bills, so long as you include the cost for each separate visit.

Medical bills prove the cost of your injury treatments. You’ll also need copies of your medical records to connect your injuries to the slip and fall, and to justify the cost and duration of your treatments. You can send a written request for both bills and records to each of your medical care providers.

Watch out if the adjuster asks you to sign an authorization that lets them request your bills and records. Never sign a blanket release form that lets the insurance company get your personal medical history for the last five or ten years. If you agree to sign a medical authorization, make sure it’s limited to records about your slip and fall injuries.

Insurance adjusters will sift through your medical bills and records to find any excuse to reject or minimize your claim.

Keep in mind that insurance companies are only legally obligated to pay reasonable and necessary medical costs. Avoid using “accident doctors” who will pump up your medical costs by ordering repeated tests or medically questionable treatments. You could easily be stuck paying medical bills rejected by the insurance company.

Capture All Out-of-Pocket Expenses

Your copays and deductible won’t be added into your damages total because they’re included in the total cost of your medical bills. Any other injury-related out-of-pocket costs will count toward your damages total so long as you have receipts or other documentation to back them up.

Save your receipts for over-the-counter medications, bandages, elastic wraps, and other medically necessary items.

If your doctor agrees there is a need, you can seek reimbursement for the cost of home medical equipment like a hospital bed, bedside commode, walker, shower chair, and more.

Collect receipts or track mileage for travel costs to medical appointments. Carfare for taxicabs or rideshare services are also legitimate expenses. If your injury requires specialized treatment far from home, transportation expenses might include food and overnight lodging for you and a traveling companion.

Be sure to get dated receipts for replacement services, meaning paying someone else for activities you would have done yourself but for your slip and fall injuries. Replacement services might include childcare, snow shoveling, dog walking, and house cleaning.

Lost Wages Verification

Ask your employer for a written statement or letter that details your wages and the days you missed from work after the slip and fall. The wage statement should list any sick leave or vacation hours you had to use during your absence. You’ll also want verification of lost performance bonuses or overtime caused by your absence from work.

If you suffered a loss of income after a slip and fall you can still seek wage reimbursement if you’re self-employed. Gather your prior year’s tax returns, profit-and-loss statements, and other evidence to show the drop in your income after the slip and fall accident.

Copies of correspondence, including emails, can be used to illustrate freelance work missed or opportunities lost because of your injuries.

The insurance company will not pay for lost wages unless you have a doctor’s note corresponding to the dates you were unable to work. Whether you are self-employed or work for someone else, talk to your medical providers about how your injuries impact your ability to work as you did before the slip and fall.

As you collect all your evidence of hard costs, create your own claim file to organize your slip and fall paperwork. Sort your bills, letters, and other evidence in chronological order in separate sections for easy reference.